Once you have a clear understanding of your financial situation, it is possible to create a financial plan. This will help you identify your monthly expenses and set savings goals. It also allows you to pinpoint areas where you can cut back. These are some tips to help you start your plan. Every transaction that takes place in your checking bank account should be recorded. This will allow you to see a history of your spending habits. Once you have this information, you can start determining where to make adjustments to your budget.

You can find resources that will help you to create a financial program

Financial planning includes many things. Your retirement strategy, risk management plan and long-term investments plan should all be included. It should include your current income, expenses, and any debts. To create a financial plan that is tailored to your needs, both long-term and short-term, it's important to identify which debts you need to pay first. These are some resources that will assist you in creating a financial plan to meet your current needs.

A profit-and-loss statement is an important part of any business's financial plan. Also known as a profit and loss statement, the P&L explains how profitable a business is and how much it makes or loses. You can use this information to make strategic decisions for your business. These guidelines will help you get started:

In a financial plan, assets and liabilities are listed

What is the distinction between assets and liabilities when creating a financial plan for your business? Liabilities are money you owe other people or businesses. They can include deferred tax, loans, and bills. You can divide your liabilities into two groups: current and longer-term. Current liabilities are any payments you need now, like short-term debts, while long-term liability is the ones you will need in the future.

What's the difference between current and non-current assets? You will categorize assets and liabilities according their current value in a financial plan. Your current assets include cash and stocks as well as investments and real estate. Equipment, vehicles and buildings are non-current assets. Your liabilities refer to the loans you need to pay for the future.

Goals in a financial plan

When creating a financial plan, setting goals should be your first step. Each goal should have a defined time frame. You should, for instance, write down how much money you plan to invest in retirement if you are planning to retire at the age of 65. Next, structure your plan around these numbers. Setting goals helps you stay motivated. A good financial plan has many goals. Retirement is one of them. This article discusses some of the most common goals.

Saving money is the most important goal for your long-term financial goals. This means setting aside 10% to 15% of your paycheck in tax-advantaged retirement accounts. Roth IRAs, as well as traditional IRAs, are both tax-advantaged accounts. You can save money by investing in these accounts to ensure you are able to retire in a few short years. Ideally, you'll save more money than you spend, so set realistic short-term and long-term goals.

Costs associated with creating a financial planning plan

There are many factors that influence the cost of creating a comprehensive plan. The cost of creating a comprehensive financial plan will directly impact the fee. It ranged from $2250 for a comprehensive plan up to $850 for modular plans. The longer the advisor worked on your plan, the higher the fee. One client's plan took advisors on average 11.9 hours to create. The final plan will reflect this fee.

The typical hourly fee for an advisor that does not offer insurance products and services is $220. Advisors who offer investment services or insurance will typically charge more than those who plan. However, the higher fees are not indicative of advisor's expertise but reflect their perceived value. Financial planners who charge an hourly fee are charged between 1%-2% of their clients' assets. The difference in hourly fees and project-based fees is minimal.

FAQ

Who should use a wealth manager?

Anyone who is looking to build wealth needs to be aware of the potential risks.

New investors might not grasp the concept of risk. They could lose their investment money if they make poor choices.

People who are already wealthy can feel the same. They may think they have enough money in their pockets to last them a lifetime. But this isn't always true, and they could lose everything if they aren't careful.

Everyone must take into account their individual circumstances before making a decision about whether to hire a wealth manager.

Why is it important to manage wealth?

You must first take control of your financial affairs. It is important to know how much money you have, how it costs and where it goes.

You should also know how much you're saving for retirement and what your emergency fund is.

You could end up spending all of your savings on unexpected expenses like car repairs and medical bills.

How do I get started with Wealth Management?

You must first decide what type of Wealth Management service is right for you. There are many Wealth Management services available, but most people fall under one of the following three categories.

-

Investment Advisory Services: These professionals can help you decide how much and where you should invest it. They provide advice on asset allocation, portfolio creation, and other investment strategies.

-

Financial Planning Services – This professional will help you create a financial plan that takes into account your personal goals, objectives, as well as your personal situation. He or she may recommend certain investments based on their experience and expertise.

-

Estate Planning Services- An experienced lawyer will help you determine the best way for you and your loved to avoid potential problems after your death.

-

Ensure that the professional you are hiring is registered with FINRA. You don't have to be comfortable working with them.

What is a financial planner? And how can they help you manage your wealth?

A financial advisor can help you to create a financial strategy. They can help you assess your financial situation, identify your weaknesses, and suggest ways that you can improve it.

Financial planners are trained professionals who can help you develop a sound financial plan. They can help you determine how much to save each month and which investments will yield the best returns.

A fee is usually charged for financial planners based on the advice they give. However, some planners offer free services to clients who meet certain criteria.

Do I need to make a payment for Retirement Planning?

No. These services don't require you to pay anything. We offer FREE consultations so we can show you what's possible, and then you can decide if you'd like to pursue our services.

What is wealth administration?

Wealth Management is the practice of managing money for individuals, families, and businesses. It covers all aspects related to financial planning including insurance, taxes, estate planning and retirement planning.

What are the potential benefits of wealth management

Wealth management's main benefit is the ability to have financial services available at any time. Saving for your future doesn't require you to wait until retirement. You can also save money for the future by doing this.

To get the best out of your savings, you can invest it in different ways.

You could invest your money in bonds or shares to make interest. To increase your income, property could be purchased.

If you use a wealth manger, someone else will look after your money. This will allow you to relax and not worry about your investments.

Statistics

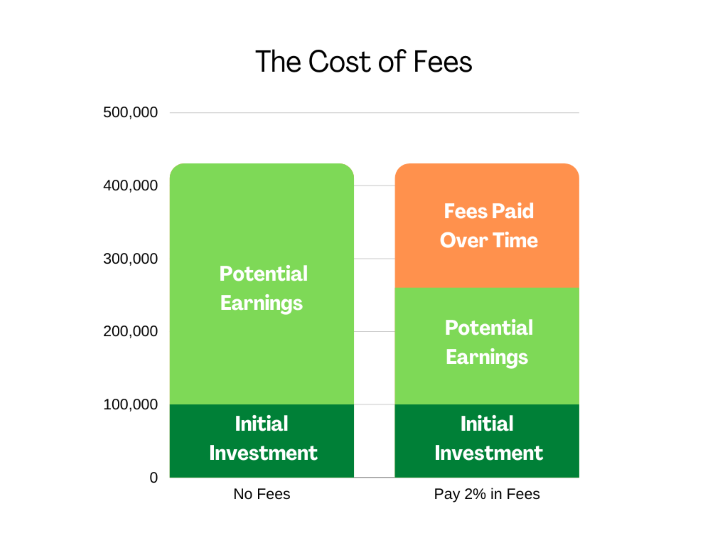

- If you are working with a private firm owned by an advisor, any advisory fees (generally around 1%) would go to the advisor. (nerdwallet.com)

- These rates generally reside somewhere around 1% of AUM annually, though rates usually drop as you invest more with the firm. (yahoo.com)

- According to a 2017 study, the average rate of return for real estate over a roughly 150-year period was around eight percent. (fortunebuilders.com)

- As of 2020, it is estimated that the wealth management industry had an AUM of upwards of $112 trillion globally. (investopedia.com)

External Links

How To

How to invest once you're retired

After they retire, most people have enough money that they can live comfortably. But how do they put it to work? While the most popular way to invest it is in savings accounts, there are many other options. You could sell your house, and use the money to purchase shares in companies you believe are likely to increase in value. You could also choose to take out life assurance and leave it to children or grandchildren.

If you want your retirement fund to last longer, you might consider investing in real estate. Property prices tend to rise over time, so if you buy a home now, you might get a good return on your investment at some point in the future. Gold coins are another option if you worry about inflation. They don’t lose value as other assets, so they are less likely fall in value when there is economic uncertainty.